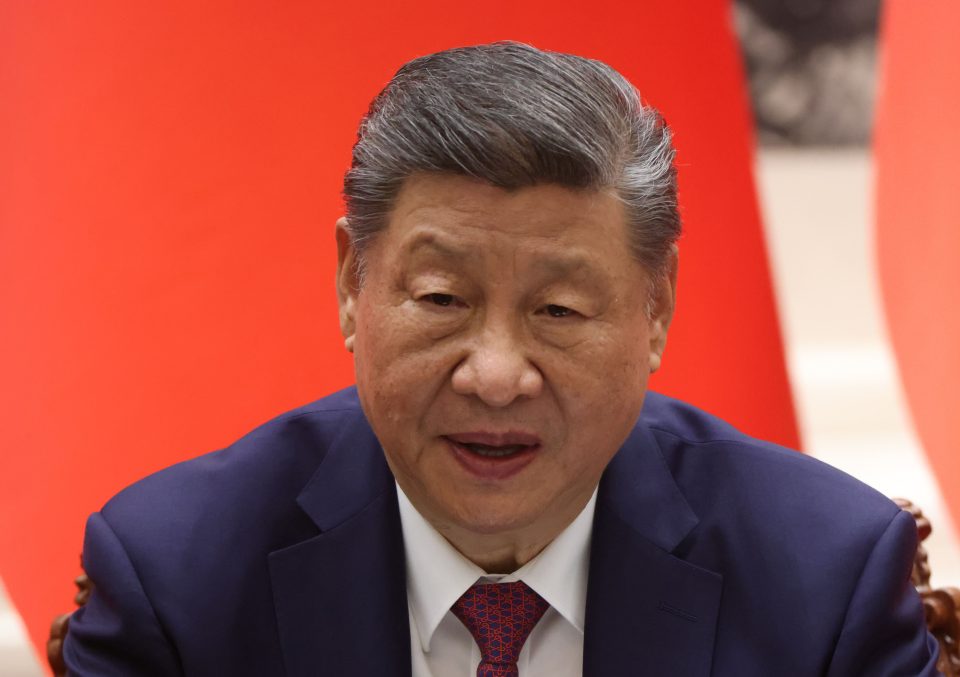

Chinese President Xi Jinping is set to travel to North Korea next week for a rare high-level diplomatic visit, a move that underscores shifting geopolitical alignments with potential implications for global trade, security risk pricing, and regional economic stability.

State media outlet Xinhua confirmed on Friday that Xi will embark on a two-day state visit starting next Monday, where he is expected to meet North Korean leader Kim Jong Un. North Korea’s KCNA also confirmed the development. The trip marks Xi’s first visit to Pyongyang since 2019 and his first overseas engagement this year.

The visit comes at a time of heightened diplomatic activity involving Beijing, following a series of high-profile meetings with global leaders, including recent engagements with US President Donald Trump and Russian President Vladimir Putin.

From a geopolitical risk perspective, the timing highlights China’s increasing efforts to position itself as a central power broker in global security discussions, particularly around the Korean Peninsula. Xi has already hosted 17 world leaders in Beijing in 2026, according to reports, reinforcing China’s expanding diplomatic footprint amid a reshaping global order.

Chinese officials have previously framed exchanges with North Korea as critical to regional stability and mutual economic interests, though analysts note that the relationship remains strategically sensitive due to sanctions, nuclear tensions, and shifting US-China dynamics.

The upcoming talks may also revive speculation around China’s potential role in facilitating broader negotiations involving North Korea’s nuclear programme, especially after renewed signals of interest from Washington in restarting dialogue with Pyongyang.

US-China discussions on the Korean Peninsula were reportedly part of recent high-level engagements between Xi and Trump, with both sides previously expressing a shared objective of denuclearisation, though progress has historically stalled.

Markets typically view developments on the Korean Peninsula through the lens of geopolitical risk premiums, particularly in Asia-Pacific equities, defence sectors, and energy supply chains, where any escalation or diplomatic breakthrough could influence investor sentiment and regional stability outlooks.